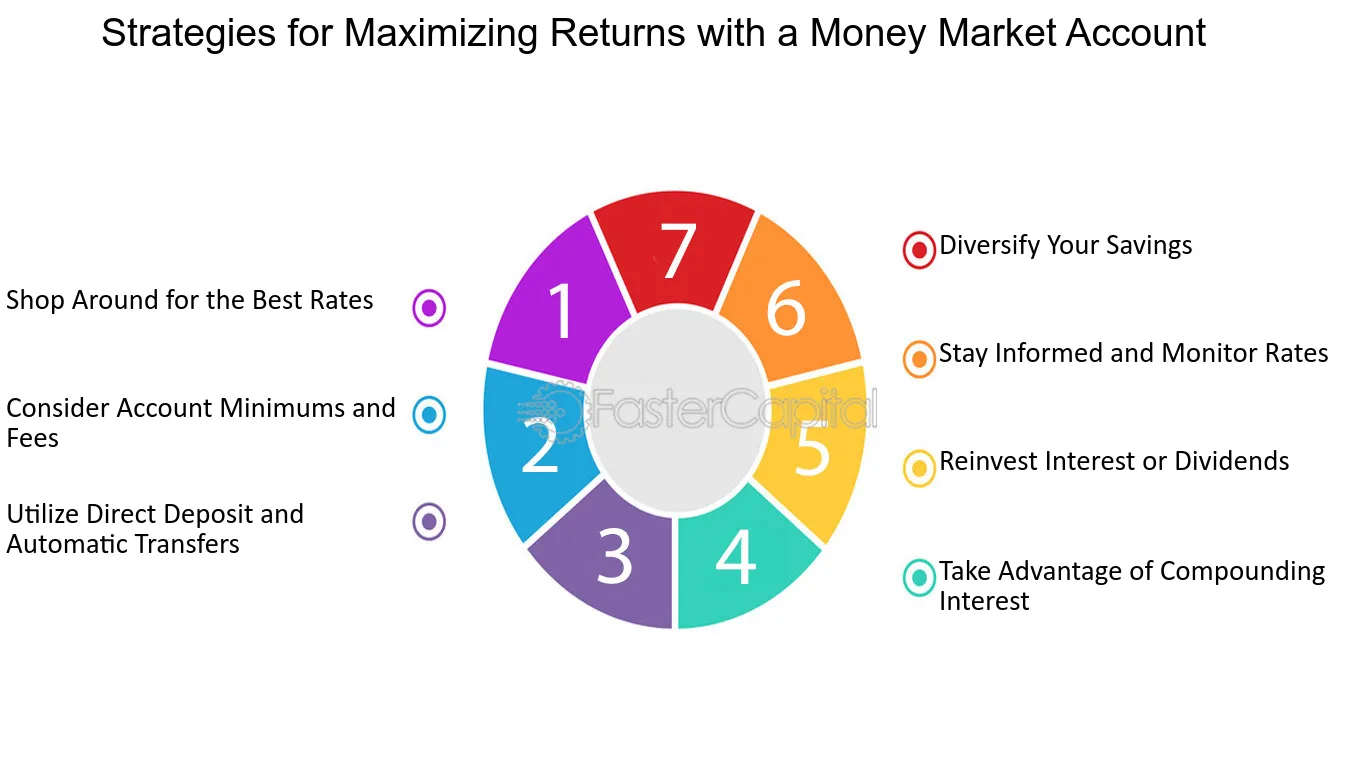

Maximizing Your Savings: Strategies for Building Wealth

Maximizing Your Savings: Strategies for Building Wealth

Saving money is a crucial aspect of building wealth and securing a financially stable future. However, with the rising costs of living and increasing expenses, it can be challenging to save effectively. In this article, we will explore strategies for maximizing your savings and building wealth over time.

1. Set Clear Financial Goals

Before you start saving, it’s essential to set clear financial goals. What do you want to achieve? Do you want to save for a down payment on a house, pay off debt, or build an emergency fund? Having a clear goal in mind will help you stay focused and motivated to save.

2. Create a Budget

Creating a budget is a crucial step in maximizing your savings. A budget helps you track your income and expenses, identify areas where you can cut back, and allocate your money effectively. Make sure to include a category for savings and stick to it.

3. Prioritize Needs Over Wants

It’s essential to prioritize your needs over your wants. Pay essential bills such as rent/mortgage, utilities, and food first, and then allocate money for discretionary spending. Avoid impulse purchases and focus on saving for the future.

4. Automate Your Savings

Automating your savings is a great way to ensure that you save consistently. Set up automatic transfers from your checking account to your savings or investment accounts. This way, you’ll ensure that you save a fixed amount regularly, without having to think about it.

5. Take Advantage of Employer Matching

If your employer offers a 401(k) or other retirement plan matching program, take advantage of it. Contribute enough to maximize the match, as it’s essentially free money that can add up over time.

6. Invest Wisely

Investing your savings can help you build wealth over time. Consider investing in a diversified portfolio of stocks, bonds, and other assets. You can also consider working with a financial advisor to create a customized investment plan.

7. Avoid Fees and Charges

Fees and charges can eat into your savings and reduce your returns. Avoid fees by choosing low-cost index funds, ETFs, or other investment options. Also, be aware of fees associated with bank accounts, credit cards, and other financial products.

8. Build an Emergency Fund

An emergency fund is essential for covering unexpected expenses, such as car repairs or medical bills. Aim to save 3-6 months’ worth of living expenses in an easily accessible savings account.

9. Avoid Lifestyle Inflation

As your income increases, avoid the temptation to inflate your lifestyle by spending more on luxuries. Instead, direct excess funds towards saving and investing.

10. Monitor and Adjust

Regularly monitor your savings progress and adjust your strategy as needed. Review your budget, investments, and financial goals to ensure you’re on track to achieve your objectives.

Conclusion

Maximizing your savings requires discipline, patience, and a clear understanding of your financial goals. By setting clear goals, creating a budget, prioritizing needs over wants, and automating your savings, you can build wealth over time. Remember to take advantage of employer matching, invest wisely, avoid fees and charges, build an emergency fund, avoid lifestyle inflation, and monitor and adjust your strategy regularly. With these strategies, you’ll be well on your way to achieving financial stability and building a secure financial future.